Table of Content

It might even be possible to move funds from an IRA into your 401, thereby increasing the amount of money you can borrow. Work with your HR department, financial planner, and tax adviser to understand the pros and cons of that technique. Before you do anything, pause and reconsider dipping into your retirement savings. Those funds can be a significant source of money, but you'll thank yourself later if you can leave the money alone and find funding elsewhere. Things are not necessarily going to get any easier when you're older and have stopped earning an income. Julius Mansa is a CFO consultant, finance and accounting professor, investor, and U.S.

Unless you meet an exclusion — such as reaching age 59½ and having owned a Roth IRA for at least five years — withdrawing earnings will generate taxes and a 10% penalty. Many savers believe that they can take loans from IRAs, because they can borrow from other types of retirement accounts. For example, some 401 plans allow loans, but IRAs do not, and they typically cannot be pledged as collateral when you apply for a loan. If your first contribution was at least five years ago, you’re good to withdraw an unlimited amount of contributions and up to $10,000 of earnings tax and penalty-free. But with a Roth IRA, you may be able to avoid both taxes and penalties if you’ve had the account open for at least five years and use it to fund a first-time home purchase. If you don't deposit the money back into an IRA within that 60-day time frame, the amount removed will be treated as a distribution, which means it will be subject to a 10% early withdrawal penalty.

Can I Withdraw Funds Without Penalty if I Roll 401(k) Funds Into a Roth IRA?

IRA withdrawals are considered early before you reach age 59½, unless you qualify for another exception to the tax. NerdWallet, Inc. is an independent publisher and comparison service, not an investment advisor. Its articles, interactive tools and other content are provided to you for free, as self-help tools and for informational purposes only. NerdWallet does not and cannot guarantee the accuracy or applicability of any information in regard to your individual circumstances.

You can learn more about the standards we follow in producing accurate, unbiased content in oureditorial policy. For the 2022 tax year, that's $6,000, or $7,000 if you're 50 or older, rising to $6,500 and $7,500 if you're 50 or over in 2023. If you don't want to touch your IRA, you can borrow 50% of your 401 balance, up to a maximum of $50,000.

Rules For Withdrawing From Your Retirement Fund for a First-Time Home Purchase

Robin Hartill is a Certified Financial Planner who writes about money management, investing, and retirement planning. She has written and edited personal finance content since 2016. Robin currently leads The Penny Hoarder's personal finance advice column, "Dear Penny." Through this platform, Robin answers the questions of readers from across the United States. She decodes industry jargon, making complicated finance topics like paying taxes, managing a portfolio, and boosting a credit score easy to understand. When you've reached retirement, you can access the money you've socked away all those years in your individual retirement account. Whether you're buying a home for your primary residence or a vacation home, you won't have to worry about early withdrawal penalties on distributions from either your traditional or Roth IRA at age 66.

Real estate investing of any type is quite risky or, at best, high maintenance; for an IRA, real estate is a particularly high-risk choice. Not only may property values drop rather than rise, but a year of significant maintenance costs could also subject you to penalties if your income and IRA contribution limit doesn't cover repairs you can't afford to ignore. However, If you need to take a distribution from retirement savings, consider all of your options, including taking withdrawals from an IRA or delaying homebuying to save more cash. To use money in a traditional 401, you can take an outright withdrawal or a 401 loan.

Who Qualifies for the IRA Exception?

Regardless of your age, withdrawals will be taxed if you’ve had your Roth IRA for less than five years, unless you qualify for an exception. You can withdraw up to $10,000 of earnings while avoiding taxes and fees if you’re using the funds for a first-time home purchase. While those contributions are yours whenever you want them, the same can't be said for any growth in the account.

You can use your IRA nest egg to buy a home at age 66 without penalty. There are IRA rules that make things far more complicated than you might expect. Sign up and we’ll send you Nerdy articles about the money topics that matter most to you along with other ways to help you get more from your money. We believe everyone should be able to make financial decisions with confidence. On the other hand, Roth IRAs have no RMDs during the account owner’s lifetime. Vikki Velasquez is a researcher and writer who has managed, coordinated, and directed various community and nonprofit organizations.

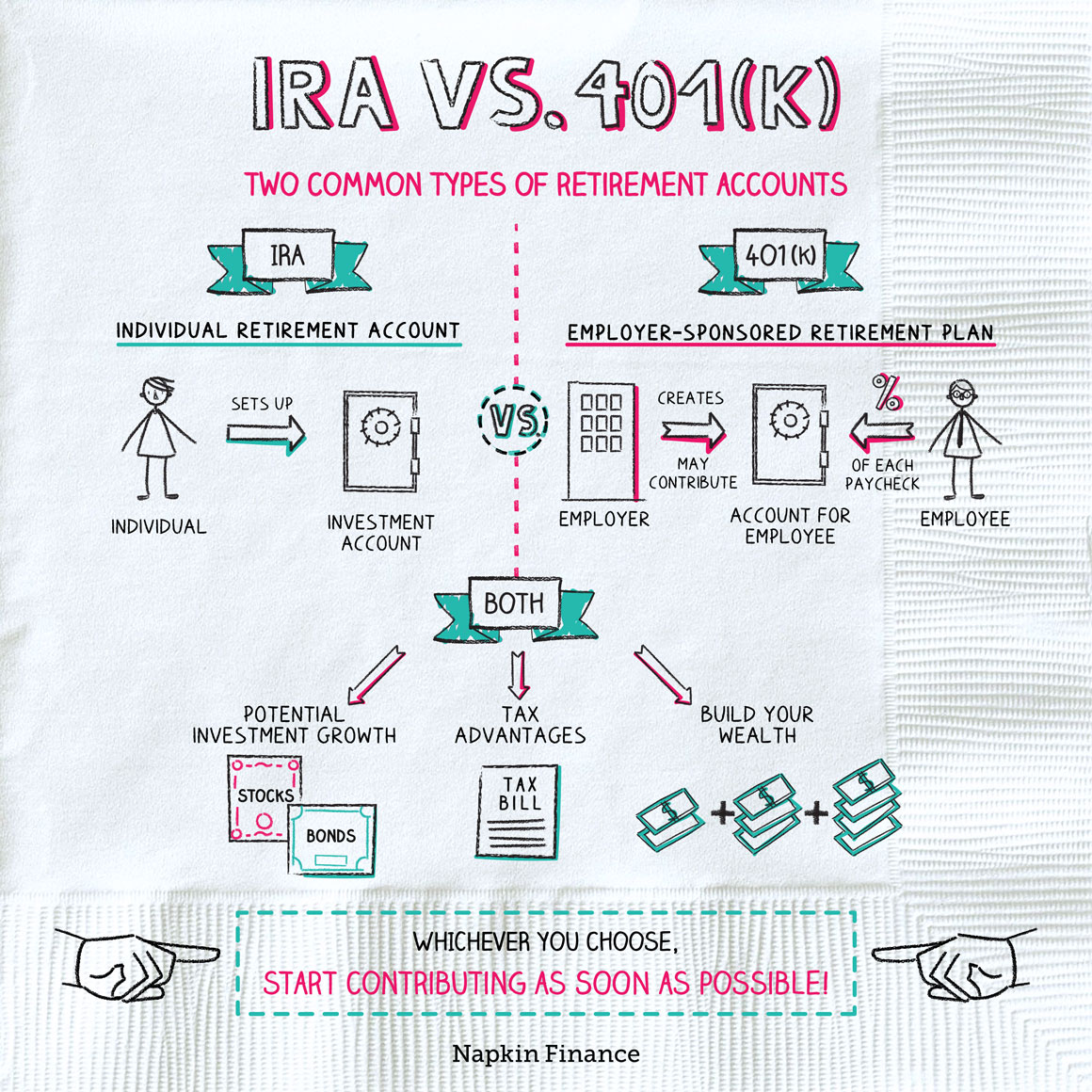

A 401 plan is a tool to help you save for retirement by offering tax advantages. With a traditional 401, you can deduct your contributions from your taxable income to lower your tax bill for the year. With a Roth 401, you make contributions with after-tax funds, then you can make withdrawals tax free, including on earnings, in retirement. When you’re buying your first home, saving up a down payment is one of the biggest challenges. One source you can turn to is your Roth IRA. A Roth IRA is an individual retirement account you fund with after-tax dollars, then make tax-free withdrawals from in retirement. In some circumstances, you can also use up to $10,000 of your Roth IRA earnings toward a home purchase without paying taxes or penalties.

Typically when you withdraw funds from a 401 before age 59½, you incur a 10% penalty. You can use your 401 toward buying a house and avoid this fee. However, a 401 withdrawal for a home purchase may not be best for some buyers because of the opportunity cost. You’ll typically owe taxes and a 10% early withdrawal penalty if you withdraw your Roth IRA earnings before reaching age 59 ½.

A non-qualified Roth IRA distribution is subject to taxes and potentially an early withdrawal penalty. Meanwhile, conventional loans may require up to 20% down, although they may offer down payment options as low as 3% to first-time homebuyers. Although the loan payments are returned to your 401, they don’t count as contributions, so you do not get a tax break nor an employer match on them. Your plan provider may not even let you make contributions to the 401 at all while you repay the loan.

And to enforce that, you'll normally owe a 10% penalty on the amount you withdraw early, along with income taxes. To avoid paying income taxes on Roth IRA distributions of earnings, you need to meet the five-year rule, even if you’re using the money to purchase your first home. However, because traditional IRA withdrawals are taxable, no five-year rule applies. A retirement plan loan must be paid back to the borrower’s retirement account under the plan. The money is not taxed if loan meets the rules and the repayment schedule is followed. A plan sponsor is not required to include loan provisions in its plan.

Use of this site constitutes acceptance of our Terms of Use, Privacy Policy and California Do Not Sell My Personal Information. NextAdvisor may receive compensation for some links to products and services on this website. The final way you can buy real estate with your IRA is by using a self-directed IRA.

No comments:

Post a Comment